Flipping Houses UK: How to Cost a Refurb Before You Offer

This article is general guidance only and is not financial or investment advice. Property investment carries risk. Always consult qualified professionals before making investment decisions.

The single biggest reason house flips in the UK go wrong isn't the property market, the builder or the specification. It's the refurb cost estimate. Flipping houses in the UK with no solid idea of how to cost a refurb before you offer is how investors end up with a project that eats their profit and sometimes their capital. I've seen it happen to good people who bought well but had no real method for quantifying what they were taking on. This guide gives you that method — covering refurb scope classification, trade-by-trade cost estimation, contingency, GDV sensitivity analysis and how to use a builder's survey before you exchange.

Why Refurb Cost Is the Deal

In property flipping, there are three variables that determine profit: purchase price, refurb cost and sale price. Of these, purchase price is negotiable, sale price is determined by the market, and refurb cost is the one you have the most control over — but only if you quantify it accurately before you commit to a purchase.

The problem is that most first-time flippers approach the purchase decision emotionally and the refurb estimate lazily. They fall for the property at the right purchase price, get a vague builder's opinion during the viewing, and proceed on optimism. The accurate refurb cost only becomes clear once they're committed — by which point it's too late to renegotiate.

The professional approach is the reverse. You cost the refurb first, based on what you can see, and let the maximum offer price follow from the numbers — not the other way around.

Classifying the Refurb Scope

Before you build any numbers, you need a clear-eyed view of what the property actually needs. That starts with scope classification.

| Scope level | Typical work | Indicative timeline |

|---|---|---|

| Light | Full decoration, carpets and flooring, minor repairs, clean-out, garden tidy | 4–8 weeks |

| Medium | New kitchen, new bathroom(s), full decoration, flooring, likely boiler replacement, some electrical and plumbing work | 8–16 weeks |

| Heavy | Everything in medium plus: structural works, full rewire, full re-plumb, damp treatment, roof work, new windows, major fabric repair | 16–28 weeks |

Classify honestly based on what the property needs — not what you'd like it to need. The photos and floor plan from the listing give you the initial read. A site visit refines it.

I've learned to be sceptical of properties that look like a medium refurb but have some heavy-scope indicators — old electrics, no central heating, visible damp, roof issues in the photos. Those are almost always heavy refurbs once you get into them. Budget accordingly.

Trade-by-Trade Cost Reference

Once you've classified the scope, break it down trade by trade. This is the only way to build a credible estimate. A single-line "refurb cost" is not a budget — it's a guess with confidence around it.

| Trade / element | Typical UK range (2025) | Notes for flippers |

|---|---|---|

| Kitchen (supply and fit) | £6,000–£20,000 | Trade/mid spec for a flip; don't over-specify |

| Bathroom (supply and fit) | £4,000–£10,000 | Per room; en suite slightly less |

| Full rewire | £4,500–£10,000 | 3-bed house; certification required for sale |

| Boiler and heating | £2,500–£7,000 | New boiler only vs. full system replacement |

| Plastering (full skim) | £3,000–£7,000 | 3-bed house; condition-dependent |

| Flooring throughout | £2,500–£8,000 | LVT or engineered wood for resale appeal |

| Decoration (full) | £2,000–£5,000 | Labour; materials add £500–£1,500 |

| Windows (full replacement) | £4,000–£9,000 | FENSA certificate required |

| Roof (repairs) | £800–£5,000 | Full re-roof: £6,000–£14,000+ |

| Damp treatment | £1,500–£6,000+ | Rising damp can be significantly more |

| Structural (wall removal, steel) | £3,000–£15,000+ | Needs structural engineer spec first |

| External/landscaping | £1,000–£5,000 | Kerb appeal matters for resale value |

| Skip hire and waste | £500–£2,000 | Often underestimated; budget per skip |

| Building control fees | £500–£2,000 | Required for rewire, extension, structural |

Add up only the trades that apply to your property. Don't include costs for work you genuinely don't need — but don't optimistically exclude a trade just because it's expensive.

If you want to speed up the floor plan to budget calculation stage, RenoCalc handles the trade-by-trade breakdown automatically from the estate agent floor plan. It applies current UK rate data and produces a structured estimate you can use as the starting point for your deal appraisal.

Contingency: What It Is and Why It's Not Optional

Every refurb on a UK property needs a contingency. This isn't builder's padding — it's an honest acknowledgement that renovation projects reveal surprises and surprises cost money.

How to size contingency for a flip

| Stage | Recommended contingency |

|---|---|

| Pre-visit estimate (floor plan and photos only) | 25–30% |

| After site survey, before full trade quotes | 15–20% |

| After detailed trade quotes on a surveyed property | 10–15% |

| Pre-1970 property or significant structural works | Minimum 15% at any stage |

Never treat contingency as money you expect to save. It's money you should plan to need. If the contingency doesn't get used, treat it as a better-than-expected outcome — not evidence that your original estimate was too conservative.

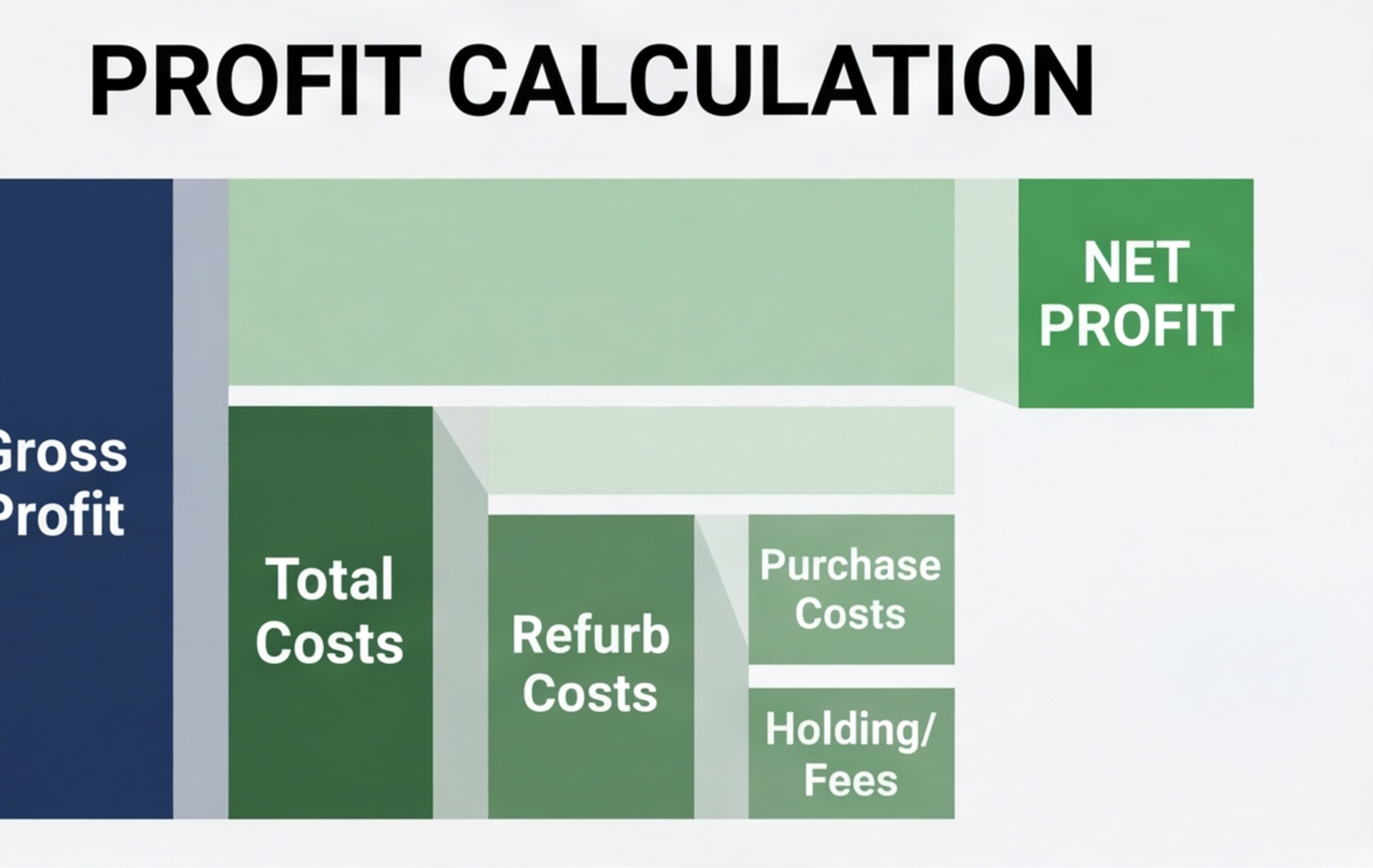

GDV Sensitivity Analysis

GDV — Gross Development Value — is what the property is worth once the renovation is complete. For a flip, this is effectively your sale price, and getting it wrong is one of the most expensive mistakes in property investing.

Why sensitivity analysis matters

Most investors run their deal appraisal on a single GDV estimate: "This street sells for £220,000 so my GDV is £220,000." That's a point estimate with no margin for error. What happens if the market softens by 5% while you're on site? What happens if the property takes longer to sell and the comparables move?

A sensitivity analysis runs the numbers at multiple GDV points:

| Scenario | GDV | Build cost | Purchase + costs | Gross profit |

|---|---|---|---|---|

| Best case | £230,000 | £38,000 | £155,000 | £37,000 |

| Base case | £220,000 | £42,000 | £155,000 | £23,000 |

| Downside | £210,000 | £48,000 | £155,000 | £7,000 |

| Stress test | £200,000 | £55,000 | £155,000 | −£10,000 |

The question isn't just whether the base case works — it's whether the downside scenario is acceptable. If the deal only works on best-case GDV and best-case build cost simultaneously, it doesn't have enough margin for the reality of property renovation.

A deal worth doing should still leave a reasonable profit in the downside scenario. If it doesn't, you need either a lower purchase price, a tighter build cost or a better GDV justification before you proceed.

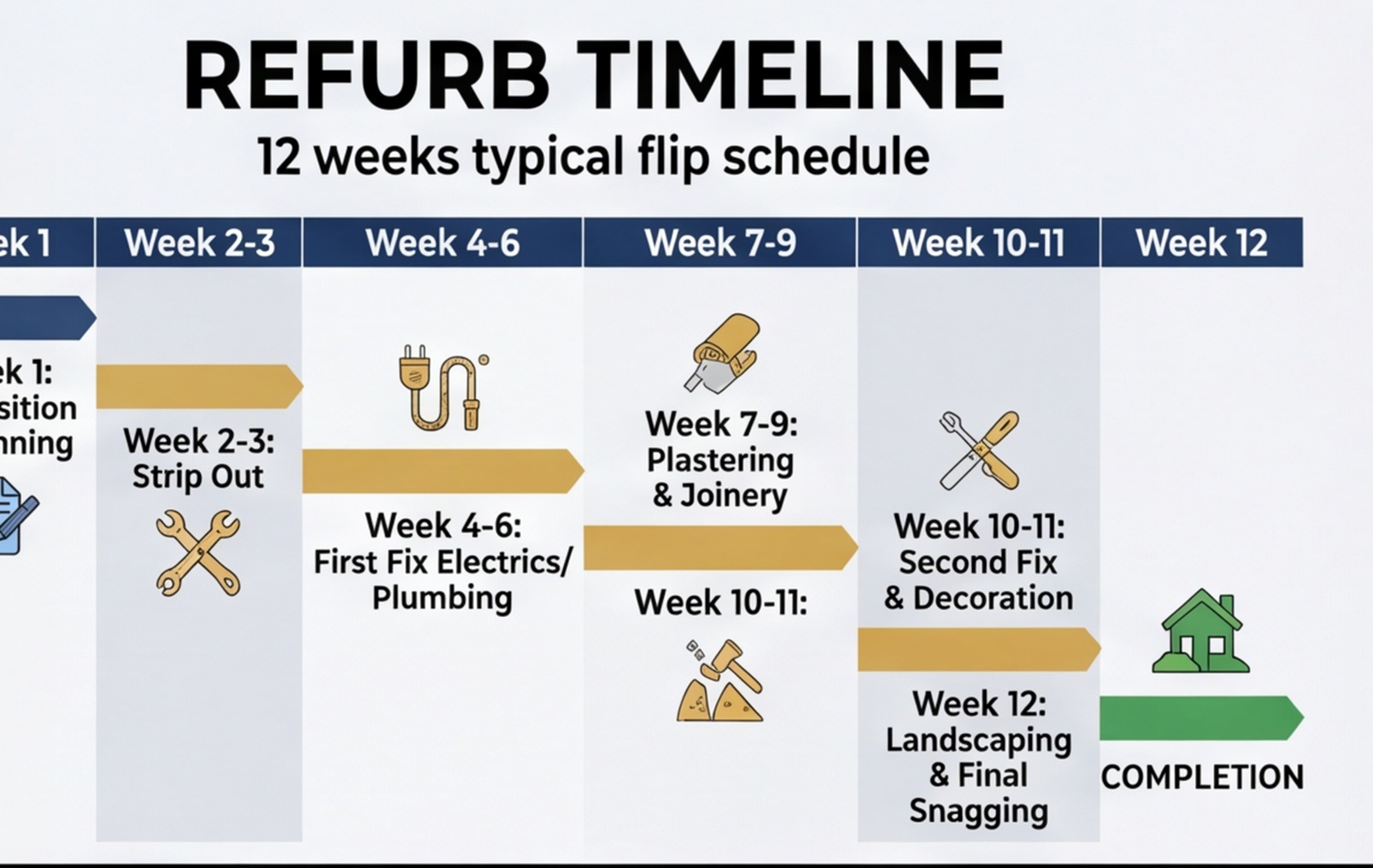

Timeline and Its Effect on Your Numbers

Most investors underestimate how much timeline affects profit on a flip. Finance costs — whether bridging finance, a development loan or the opportunity cost of your own capital — accrue every month the project runs.

A simple example: if you're paying 0.75% per month on a bridging loan against £155,000, that's £1,162 per month in finance cost. An 8-week overrun adds around £2,300 to your cost base — equivalent to a significant overspend on a trade package.

Timeline risk factors to build into your planning:

- Planning permission — even for small extensions, allow 8–13 weeks from application

- Structural engineer sign-off — typically 2–4 weeks after survey

- Asbestos removal — if found on strip-out, this causes programme disruption

- Material lead times — kitchens, windows and staircases often have 4–8 week lead times

- Trade availability — good tradespeople are busy; last-minute programme changes are expensive

- Building control inspections — inspectors need notice; failed inspections cause re-work

Build the realistic programme into your deal appraisal. If the deal only works on a 12-week timeline but the realistic estimate is 18 weeks, you need to price that difference before you commit.

Getting a Builder Survey Before Exchange

For any significant flip — anything beyond a light decoration job — I'd strongly recommend getting a builder's survey before you exchange contracts. This is different from the formal RICS survey you'll likely get for your lender. A builder's survey is a detailed walkthrough with a contractor to identify the scope, verify your estimates and flag anything that would change the numbers.

What to bring to the builder's survey

- Your scope notes from the initial assessment

- Your working cost estimate, so the builder can challenge it

- A specific list of questions about anything you're unsure of

- A camera — photograph everything the builder points out

What the builder should tell you

- Whether your scope classification is right

- Whether any structural works are needed that weren't obvious

- Their rough assessment of condition — electrics, heating, roof, damp

- Any concerns about access, party walls or planning implications

- A broad cost indication that you can check against your estimate

This survey is not a formal tender — it's a sense-check. The formal fixed-price quote comes later, once you have full access and a detailed spec. But getting a builder on site before exchange means you won't exchange on a property whose true refurb cost is 40% higher than your estimate.

Use RenoCalc to generate a structured scope document from the floor plan before the builder's survey. It gives the builder something specific to challenge or confirm, rather than starting from scratch on a blank sheet.

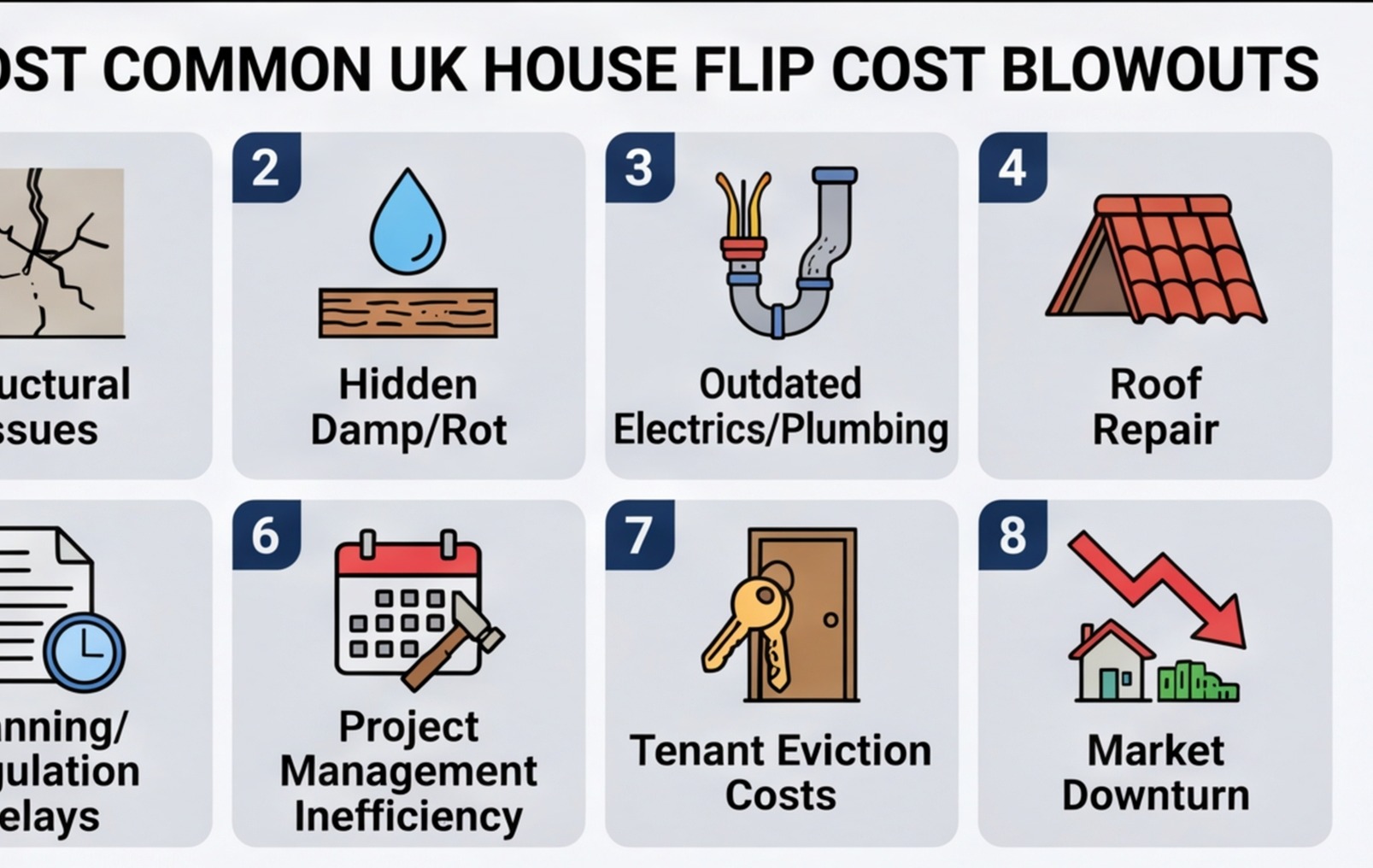

The Most Common Cost Blowouts on UK Flips

I've been in and around building projects for 30 years. These are the costs that catch flippers out most often:

1. Electrics worse than expected

A fuse board with rewirable fuses or a consumer unit with no RCDs looks manageable until the first fix electrician opens the walls and finds rubber-sheathed wiring from the 1960s. A partial rewire becomes a full rewire. Budget for a full rewire on any property built before 1990 unless you have solid evidence the electrics are already compliant.

2. Damp that was masked

Freshly painted walls hide a lot. Damp can be hidden behind bathroom panels, under carpets or behind plasterboard that was put up to conceal a problem rather than fix it. Factor in a damp check as part of every site visit — a moisture meter costs £30 and can save you thousands in surprises.

3. Asbestos

Properties built before 1990 may contain asbestos in textured coatings (artex), floor tiles, pipe lagging and roof materials. You won't know until you start stripping. An asbestos survey (typically £200–£400) before work starts is worthwhile on any pre-1990 property. Removal of asbestos-containing materials can add thousands to your cost base and weeks to your programme.

4. Structural costs from wall removals

Removing a wall to open up a kitchen-diner sounds straightforward. It usually isn't. Structural engineer's calculations, a temporary works design, RSJ supply and fit, padstones, building control inspections and making good — what looks like a £2,000 job often lands closer to £6,000–£10,000 for a standard mid-terrace ground floor wall removal.

5. Specification creep

This is the flip killer nobody talks about. You start with a mid-spec kitchen. Then the investor decides to upgrade the units. Then the worktop. Then the splashback tiles. Every decision on its own is small. Collectively they can add £5,000–£10,000 to a kitchen budget and repeat across every room in the property. Set a specification before you start and enforce it.

For more detail on using floor plans to build your early estimate, read our guide on turning a Rightmove floor plan into a renovation budget. If you're running a BRRRR strategy rather than a flip, the approach to refurb costing is similar — see our BRRRR strategy UK guide for detail on how refinance risk changes the calculation.

Frequently Asked Questions

Is flipping houses in the UK still profitable in 2025?

It can be, but margins have tightened compared to the 2010s. Higher purchase costs (stamp duty surcharge for additional properties), increased build costs and a more cautious mortgage market have all squeezed returns. The deals that still work in 2025 are typically distressed or below-market properties where the discount on purchase is wide enough to absorb refurb costs and still leave a worthwhile profit. Accurate pre-purchase refurb costing is more important than ever. This article is general guidance only and not financial advice.

What is the 70% rule in house flipping?

The 70% rule is a quick deal-screen used by property flippers: don't pay more than 70% of the after-repair value (ARV) minus your estimated renovation costs. So if a property has an ARV of £200,000 and renovation costs of £30,000, the maximum purchase price would be (£200,000 × 0.70) − £30,000 = £110,000. It's a rough guide rather than a precise model, and it doesn't account for all purchase costs, finance or holding costs. Treat it as a first filter, not a deal appraisal.

How do I cost a refurb before I've had full access?

Start with the estate agent floor plan and listing photos. Extract the total floor area, count wet rooms and classify the refurb scope as light, medium or heavy. Apply current UK trade rate ranges to each category, add a 20–25% contingency for unknowns, and you have a working pre-access budget. Tools like RenoCalc can generate this from the floor plan image in minutes. Once you have access, run a proper site survey to refine the estimate and reduce contingency.

What are the most common reasons house flips go over budget?

The main culprits are: underestimated structural costs (rotten lintels, wall movement, bad foundations), electrical rewires that were thought unnecessary but turned out to be essential, damp that was worse than visible, asbestos found on strip-out, delayed timelines that increase finance and holding costs, and specification creep — where the fit-out gets upgraded mid-project. A realistic contingency and a fixed-price contract where possible are the best protections against all of these.

How long does a house flip take in the UK?

A light refurb can take 4–8 weeks. A medium refurb — new kitchen, new bathroom, full decoration — is typically 8–16 weeks. A heavy refurb involving structural works, rewire, re-plumb and full fit-out can take 16–26 weeks or more. Timeline directly affects your finance costs, so optimistic programme estimates are expensive. Budget for the realistic timeline, not the best-case one.

Should I manage the flip myself or use a main contractor?

Self-managing gives you more control over costs but requires significant time, trade management experience and the ability to sequence and coordinate contractors. A main contractor charges a margin (typically 10–20% on top of trade costs) but handles sequencing, problem-solving and programme management. For a first flip or a property that's far from where you live, a main contractor often makes more sense financially once you factor in your own time cost. For experienced investors running multiple projects, self-management with a trusted subbies network can be more cost-effective.

Get the Refurb Cost Right Before You Offer

Flipping houses in the UK with a solid refurb cost estimate puts you in control of the deal. It tells you exactly what you can pay, what contingency you need, and whether the profit margin holds up when the market moves. Do the work before you offer. If the numbers don't work, walk away — there's always another deal.

If you want a fast, reliable refurb cost estimate from the floor plan before your viewing, try RenoCalc — upload the Rightmove floor plan and get a trade-by-trade budget in under 3 minutes.

Cost the Refurb Before You Make an Offer

RenoCalc turns any estate agent floor plan into a detailed renovation budget in under 3 minutes. Get your numbers right before you negotiate.

Get Your Refurb Estimate

Pindi Sahota

Pindi has spent 30+ years in the building trade, running building projects across the UK. He is the founder of RenoCalc — the AI quoting app that turns floor plans into full job quotes in under 3 minutes. Based in Coventry, Director of Future Build Cov Ltd.